The Social Security program is in need of significant changes, and this could have significant impacts on retirement planning. The funding for the Social Security Trust will run out of money between 2032 and 2035 if no adjustments are made. As the aging population swells, and workforce participation declines, the ratio of contributors to beneficiaries isn’t sustainable. That is why lawmakers will have to negotiate with one another to reduce benefits for future retirees and increase current earners’ taxes.

However, you don’t have to worry about federal retirement benefits because there are steps you can take. First, don’t panic that Social Security benefits will disappear entirely. The program may still have some value but have less cash flow in retirement. You can build assets throughout your working life to turn it into income during your retirement years. With a quantifiable savings strategy, discipline, and a plan for distributing savings, most of us can reach our financial goals.

The first step towards effective retirement planning is having a high saving rate. The majority of households should aim to save 15%-20% of their net income or might even need to save even more to make up for a possible drop in Social Security benefits. To boost your savings rate, budget and monitor your income each month, set aside a predetermined share of each paycheck to a savings or investment account, and take advantage of retirement plans and employer contribution matches.

Once you have accumulated assets, they need to be invested responsibly for growth. Your portfolio allocation should change as your retirement investment timeline changes, and the 4% rule is an essential consideration to take note of. It asserts that retirees should not spend more than 4% of their investment account each year, which could cause retirees to outlive their savings.

Distribution principles are critical considerations for those who do not have plans to depend on Social Security. Every person can have their own retirement income goals, but they will have to build up enough liquid wealth to satisfy the 4% rule. If you want $50,000 in annual distributions from an investment account in retirement, you need to have at least $1.25 million in that account.

Overall, in the face of Social Security program changes, it is essential to have a pragmatic approach towards retirement planning. To do so, you must prioritize high saving rates, responsible investment, and asset distribution that enables long-term returns while accounting for Social Security program changes.

Not surprisingly, retirees who had other forms of income besides Social Security were more likely to say they were “at least okay” financially compared to those who only collected Social Security in 2022. Of those who had earned income wages, 83% said they were doing at least okay. Seventy-eight percent of those collecting a pension said they were okay, and 87% with income from interest, dividends or rents said the same.

The best odds for doing “okay” in retirement may be combining multiple forms of passive income, based on the survey results. Of those who collected a pension plus interest, dividends, or rents, 96% said they were okay. Only 53% of retirees with no income besides Social Security said they were okay financially.

Making up for lower Social Security benefits

To reach our financial goals, most of us will have to build assets throughout our working lives so that we can turn them into income throughout retirement. This requires a quantifiable savings strategy, discipline, and a plan for distributing savings.

The first step is achieving and maintaining a high savings rate. Most households should strive to save 15% to 20% of their net income — it might need to be on the higher side to make up for a drop in Social Security benefits.

To increase your savings rate, it’s important to create a budget and track where your income goes each month. That way, you can measure progress. It might be helpful to set aside a predetermined amount of each paycheck that can systematically feed a savings or investment account. It’s also helpful to utilize retirement accounts and employer contribution matches to ensure you’re saving a decent amount before it even hits your paycheck.

As you accumulate assets, they need to be invested for responsible growth. I’m still at least 30 years away from retirement, so my priority is generating the highest possible returns within my risk tolerance. I’ll pay more attention to reducing volatility and limiting losses with bonds and dividend stocks as I approach retirement.

For now, I’m focused on a retirement investment portfolio with relatively high exposure to growth stocks and quality factors, supported by a smaller allocation to value stocks. Your portfolio allocation should evolve as your retirement investment timeline changes. This is likely to provide the highest possible long-term returns.

Distribution is the final phase of retirement planning, and it’s an important consideration if you don’t want to depend on Social Security. After you stop working, you’ll have to rely on your accumulated assets to provide cash to cover basic needs and lifestyle expenses. Financial planners have generally followed the 4% rule, which asserts that retirees can spend no more than 4% of their investment account each year. Any more than that, and they run the risk of outliving their savings.

Where is Social Security heading?

Legislators will be faced with tough decisions and negotiations about how to fix the situation and extend Social Security’s life span. The most likely outcome will result in a combination of reduced benefits for future retirees, along with higher taxes on current earners.

I’m not buying into the most extreme variety of hysteria and expecting my Social Security benefits to be zero. However, I am fairly confident that today’s recipients are enjoying more buying power with those benefits than people who retire at least 20 years from now. I’m treating it like an unknown that’s certain to contribute less cash flow in retirement.

OVERVIEW

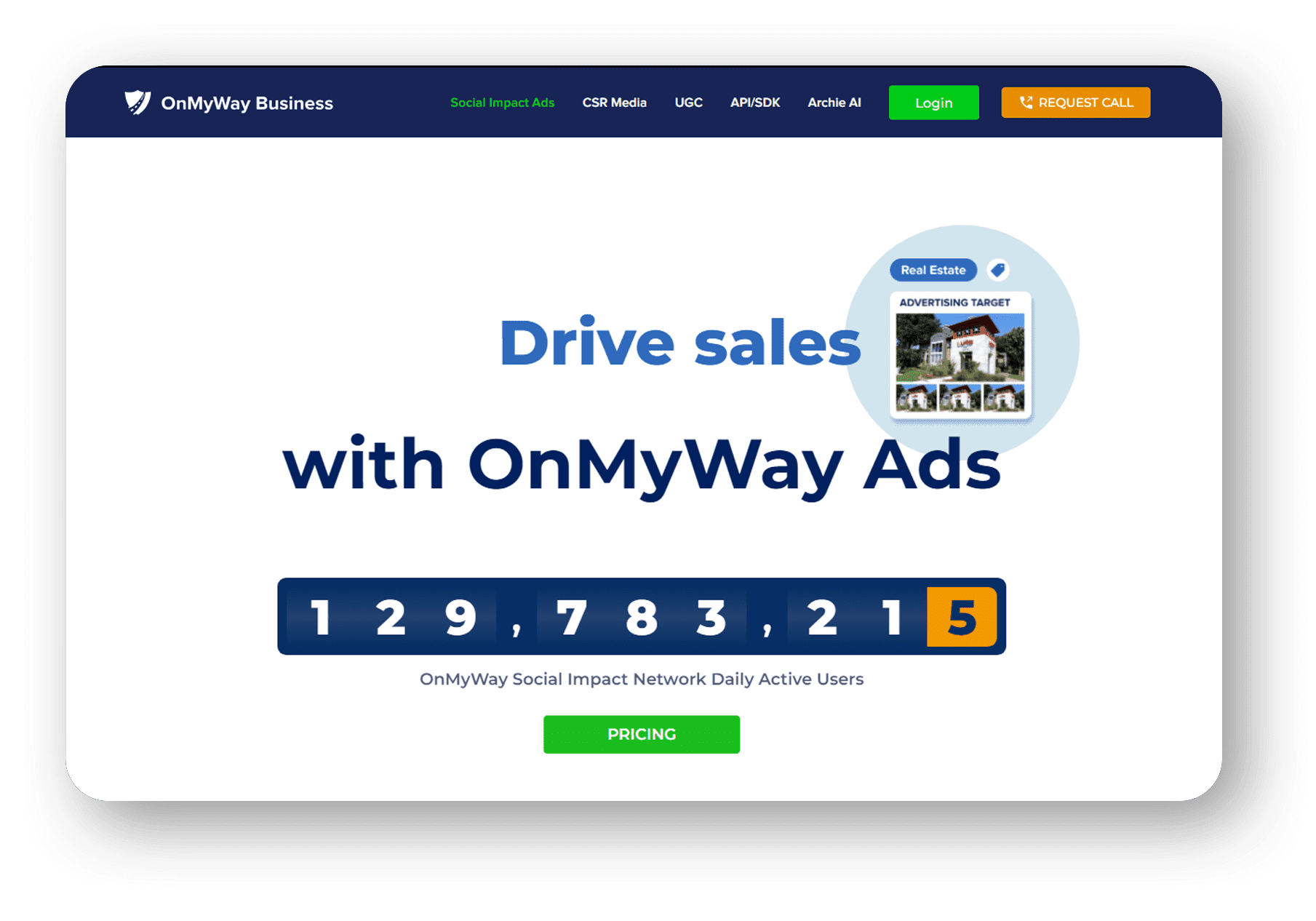

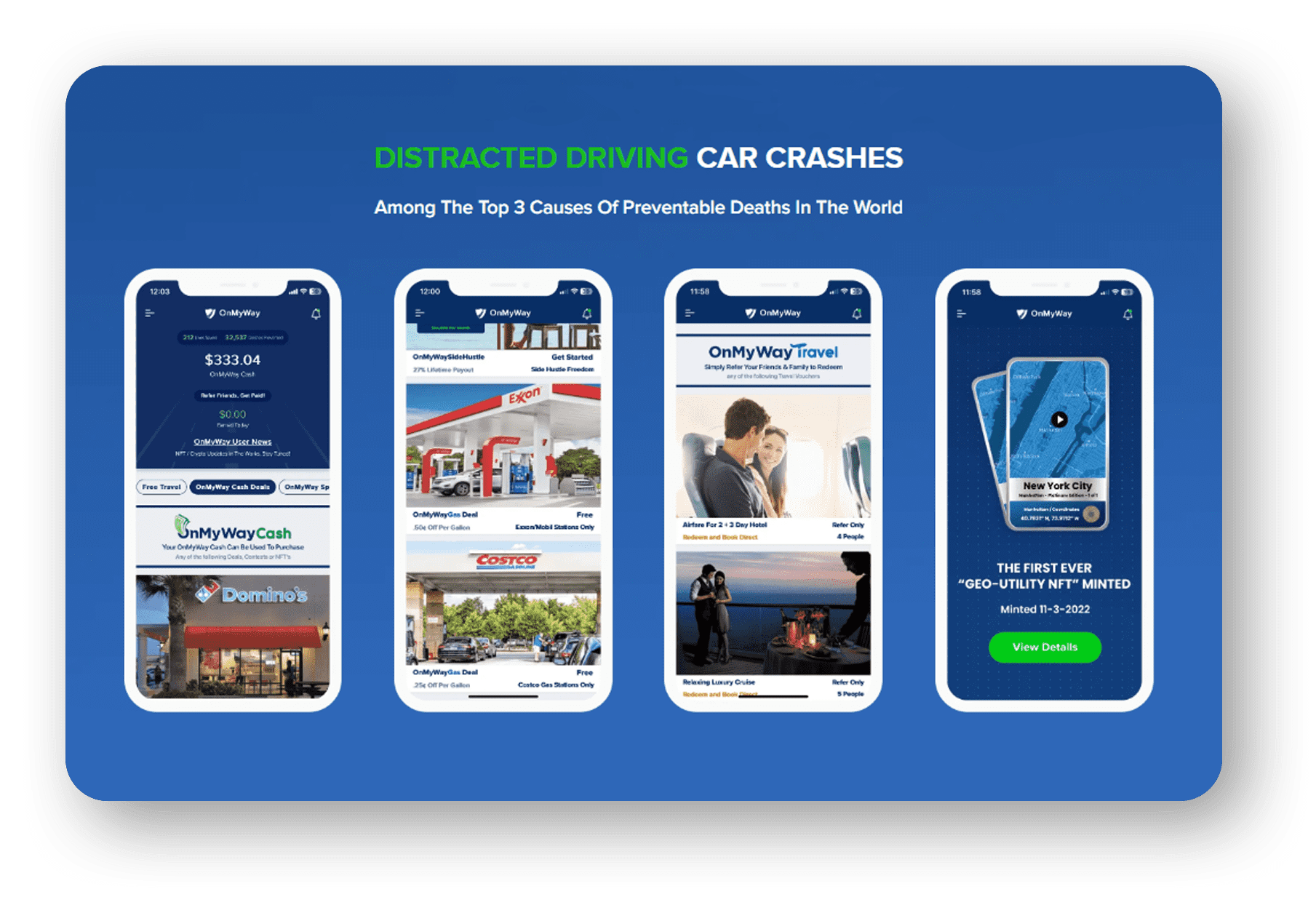

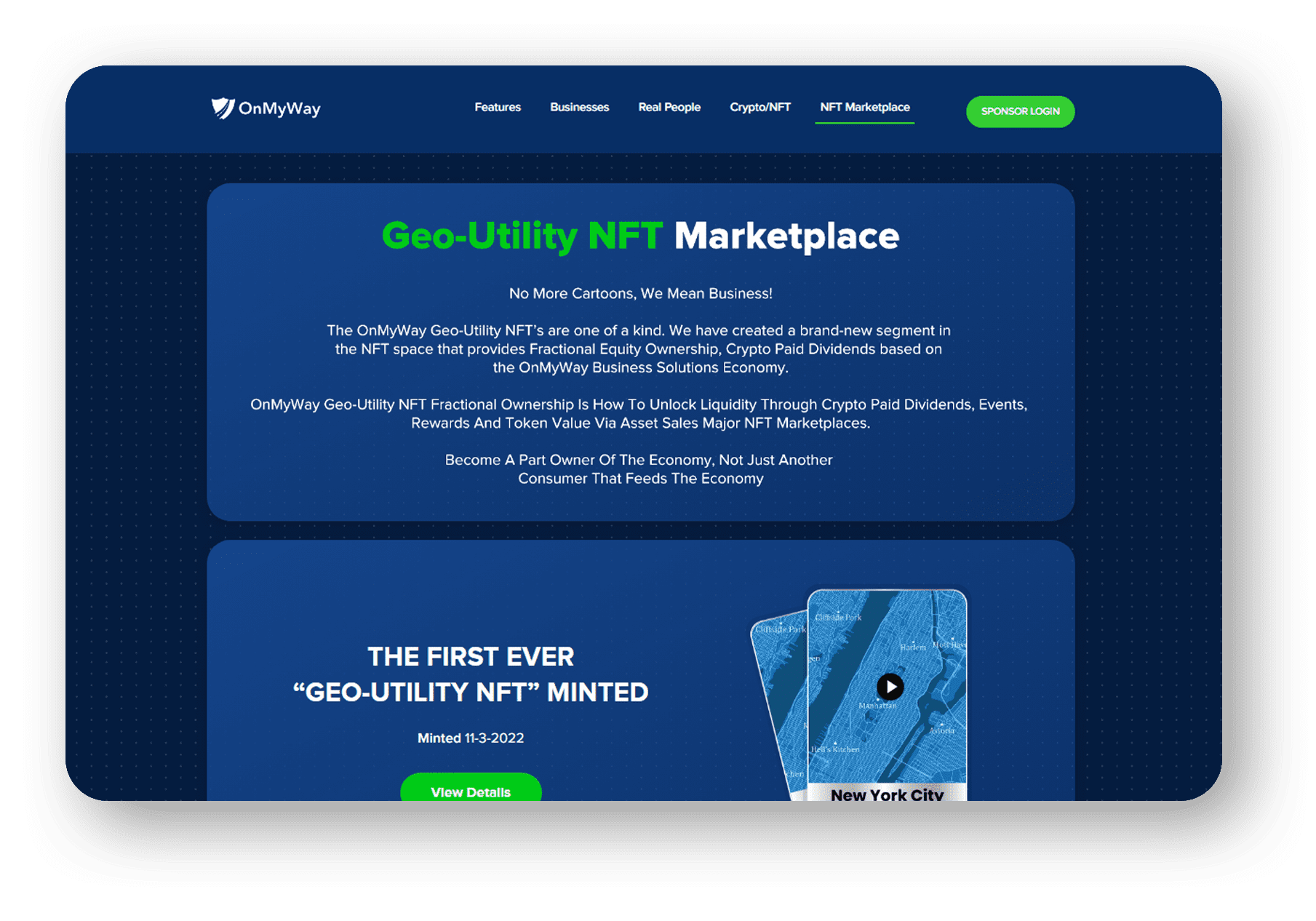

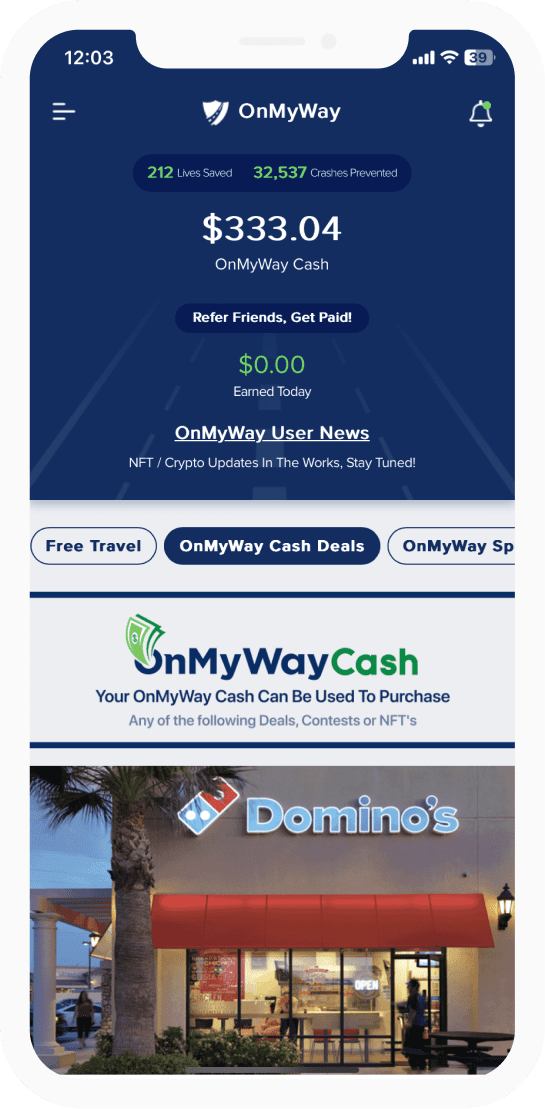

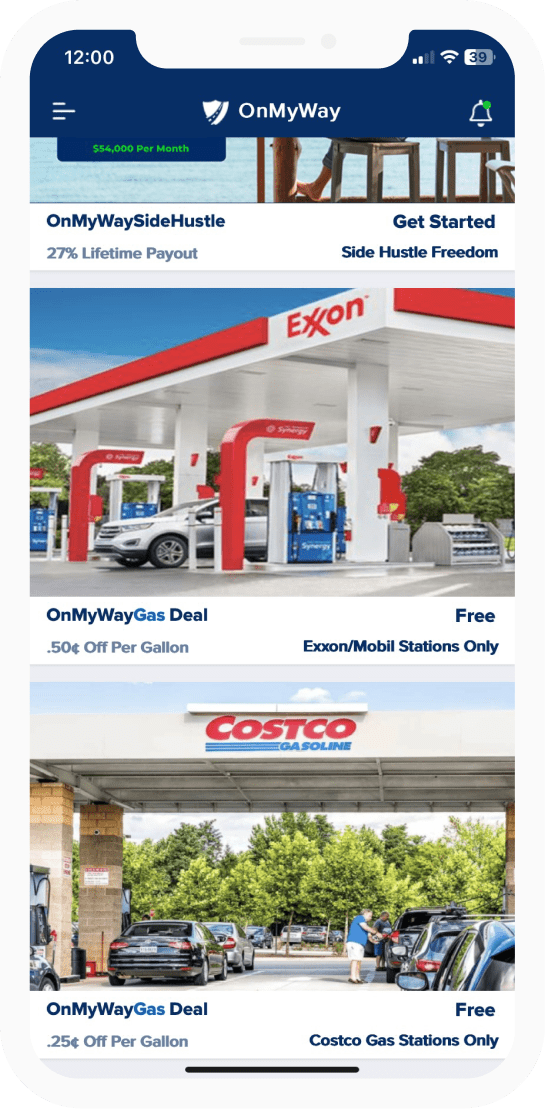

OnMyWay Is The #1 Distracted Driving Mobile App In The Nation!

OnMyWay, based in Charleston, SC, The Only Mobile App That Pays its Users Not to Text and Drive.

The #1 cause of death among young adults ages 16-27 is Car Accidents, with the majority related to Distracted Driving.

OnMyWay’s mission is to reverse this epidemic through positive rewards. Users get paid for every mile they do not text and drive and can refer their friends to get compensated for them as well.

The money earned can then be used for Cash Cards, Gift Cards, Travel Deals and Much, Much More….

The company also makes it a point to let users know that OnMyWay does NOT sell users data and only tracks them for purposes of providing a better experience while using the app.

The OnMyWay app is free to download and is currently available on both the App Store for iPhones and Google Play for Android @ OnMyWay; Drive Safe, Get Paid.

Download App Now – https://r.onmyway.com

Sponsors and advertisers can contact the company directly through their website @ www.onmyway.com

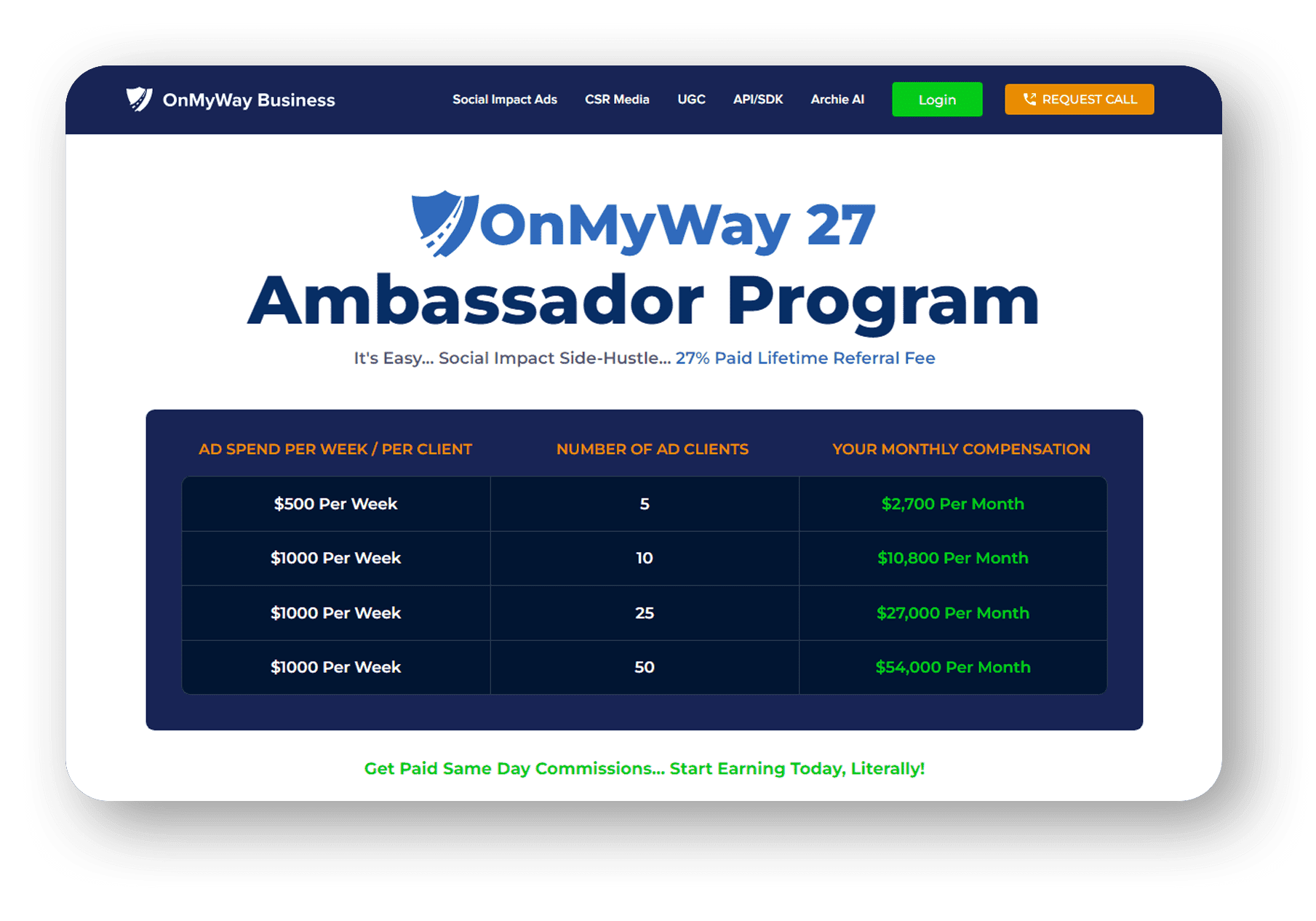

OnMyWay is the Only Texting and Driving Solution That Pays

Trusted and  By Millions of OnMyWay Mobile App Users

By Millions of OnMyWay Mobile App Users